Secure Your Financial Future Through This App

Overview

Nestify is a mobile app for managing personal finance. It’s designed specifically for millennials and Gen Z in Indonesia who:

- Struggle in maintaining their monthly cash flows.

- Having difficulty paying off their debts.

- Less financially literate.

- Having mid- and long-term goals, but feeling confused about how to achieve them.

- Want to grow their assets through investing.

I packed those five pain points into a one-stop financial management tool.

Goals

- Create a user-centered digital experience that reflects accountability, accuracy, personal data privacy & safety, and suitable financial usability.

- Design an intuitive dashboard that combines saving, cash flow transactions, and investing activities, with minimal friction in browsing, updating, customizing, and verification.

- Introduce some intuitive features:

- personalized financial scanning based on monthly income and expenditures, where users can measure their financial condition and conclude their financial wealth, equipped with detailed financial recommendations.

- my wallet and envelope system in several currencies to enable users to manage their monthly spending easily.

- goal-based setting in saving or investment with scheduled auto-debit.

- investment simulation equipped with an investment calculator and an annuity calculator, especially for purchasing a house with a KPR (mortgage) or purchasing a vehicle with an installment system.

- Nestify Pedia and Nestify GPT for users’ financial literature enrichment and consultation.

- gamification system for future app growth, emphasizing the psychological aspect of users.

- Ensure responsive design across mobile as the primary focus for executing the financial activities, and for desktop and tablet for a more detailed information and trend review.

- Establish a consistent design system inspired by functionality rather than aesthetics.

Problem

Millennials and Gen Z in Indonesia often experience the following:

- Unorganized Financial Management.

- Struggle to be disciplined for saving, investing, and even tracking expenses.

- Usually use manual recording, such as a notebook or Excel.

- Lack of Financial Consciousness

- Having difficulty being financially disciplined because lifestyle and short-term indulgences dull the importance of long-term financial goals.

- Many users feel motivated at, the beginning of their financial plans but are easily demotivated in the middle.

- Investment Confusing

- Many users (Indonesian young generation) still don’t understand the difference between real assets and liabilities, the importance of investing, and the types of instruments they can use to grow their assets.

- Users have dream goals but don’t know how to achieve them effectively, with an affordable amount of investment based on their financial condition.

Expected UX Metrics

Goal Completion Rate

Conversion Rate

Return Frequency

Drop-Off Reduction (Onboarding & Goal Setup)

Monthly Active Users

Successful Auto-Debit Execution

Time-to-Value

Key Design Decision

- Automation over manual tracking: enable inconsistent users to build a consistent habit.

- Goal-based planning as a financial anchor: more engaging than just a financial dashboard.

- MVP excludes advanced AI & investment: staging phases to launch every feature, especially for the advanced features, to avoid overwhelming users.

Core Features

- Cashflow Tracking System. Why is this important? This feature enables users to control their budget and avoid leakage of funds and financial debt.

- Auto-Debit Emergency Fund. This feature is also crucial because it builds users’ saving habits.

Constraints & Assumptions

- Constraints

- High expectation for trust and security.

- Complex features can’t be shipped at once.

- Users have several levels of financial conditions and literacy.

- Assumptions

- If the app’s security is clear, users will be willing to integrate their bank accounts.

- Automation reduces cognitive load & increases savings & investments habits.

What I Did?

As a product designer, my role is to build an end-to-end product using the design thinking approach. Here is the step-by-step process:

- Empathize:

competitive analysis, user research (survey + interviews) & synthesis (affinity mapping). - Define: synthesis (personas, value proposition canvas (VPC) – user profiles, journey map), main problem statements, and how might we.

- Ideate: Product scoping (VPC – value map, feature ideas, feature map), user flows, wireframing (low-fidelity wireframe).

- Prioritization (RICE).

- Prototyping: middle-fidelity wireframes, design system, high-fidelity UI, responsive designs, mockup designs, and interactive prototype

- Testing: usability testing (interactive prototype testing & user experience questionnaire/UEQ) and design iteration.

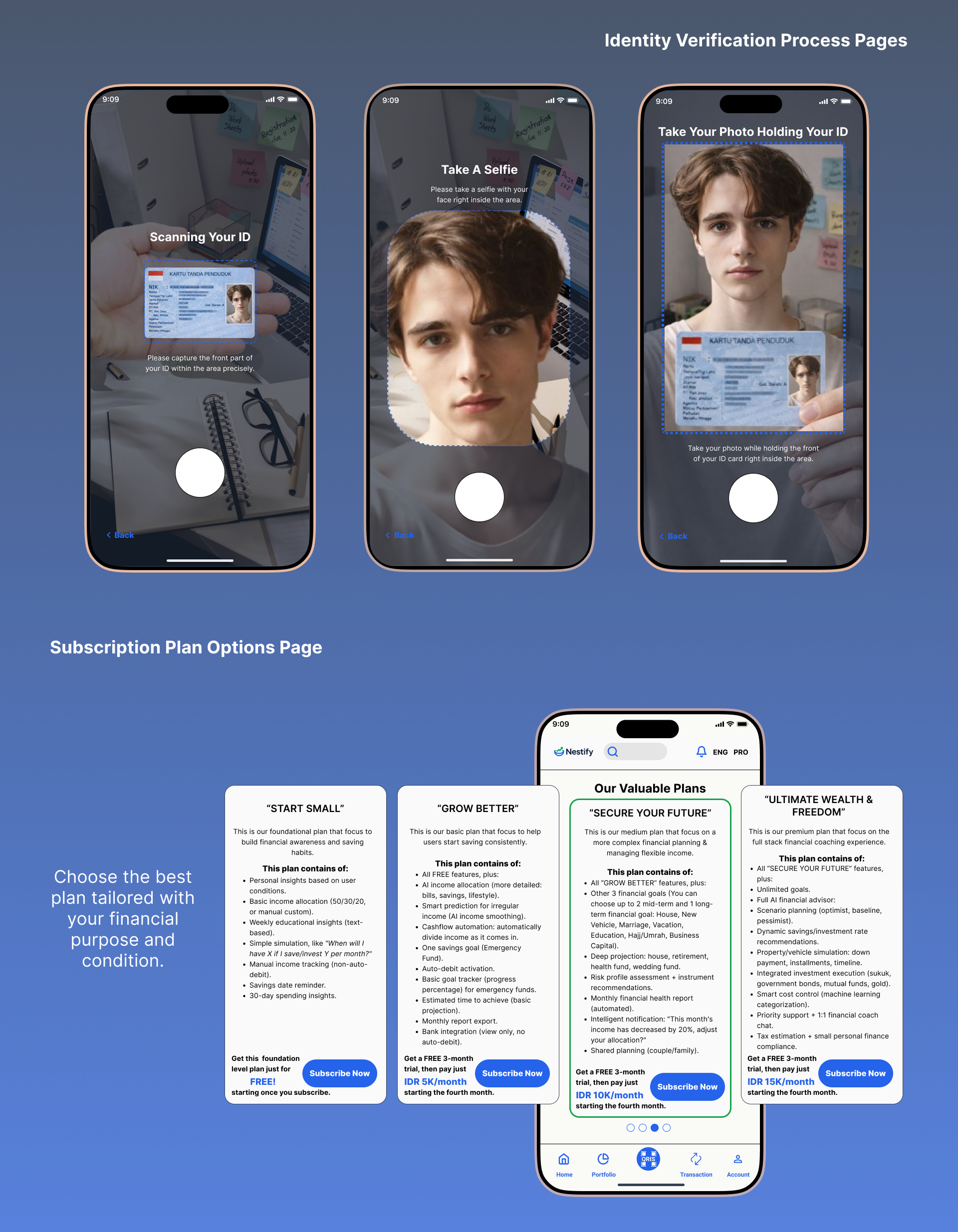

The following pictures showcase how users go through the identity verification process and choose the suitable plan before making any financial transactions through the app.

What's Next?

I expect Nestify is about to provide several interesting features down the line. They will allow users to achieve their financial goals more easily.

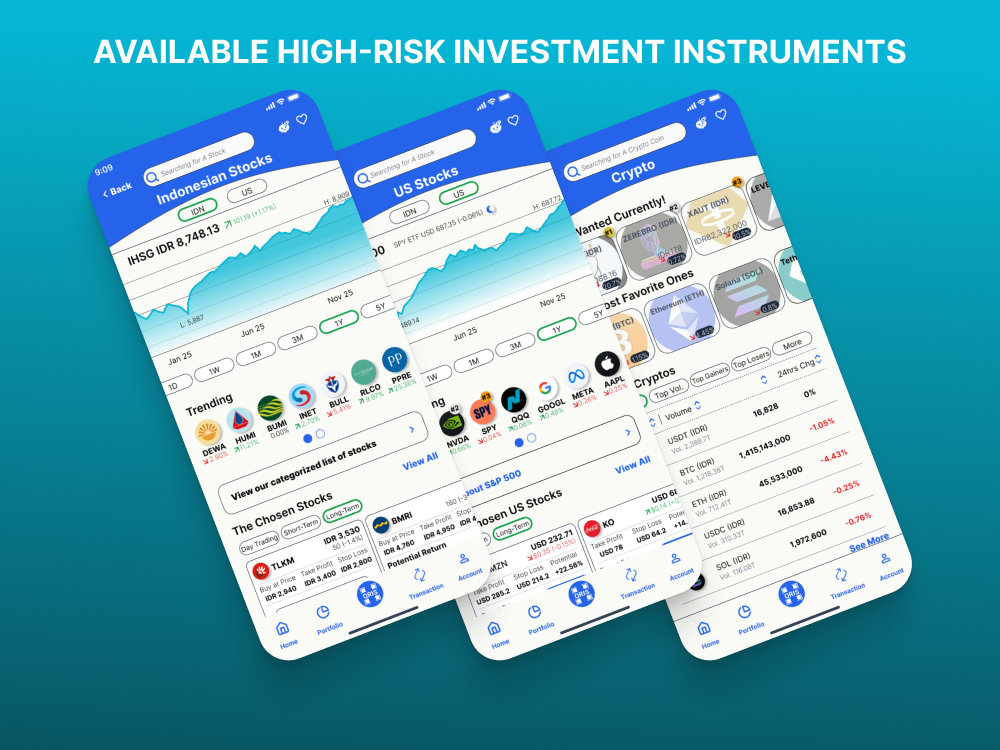

After going through several phases and with continued feature enhancements, Nestify offers several types of investment instruments, ranging from low-risk to high-risk.